- A level-funded health plan combines fixed monthly payments with the potential to recoup unused claims dollars at year-end.

- Stop-loss insurance caps your exposure. You're not taking on unlimited claims risk.

- Level funding works best for employers with 25 to 200 employees and relatively healthy workforces.

- Unlike fully insured plans, level-funded plans give you access to detailed claims data you can actually act on.

- Medical underwriting is required, and renewals can increase significantly after a high-claims year.

- How and where employees get care directly shapes your claims. Reducing avoidable ER and urgent care use is one of the most effective levers employers have under this structure.

- The carrier and virtual primary care partners you choose matter as much as the plan design itself.

A level-funded health plan sits between fully insured coverage and traditional self-funding. For employers, that means predictable monthly costs without giving up the ability to capture savings when your workforce stays healthy.

According to KFF's 2025 Employer Health Benefits Survey, 37% of covered workers at small firms are already enrolled in a level-funded plan, and that number has held steady year over year; a sign that more employers are moving toward structures that reward good claims performance.

What Is a Level-Funded Health Plan?

A level-funded health plan is a self-funded arrangement with fixed monthly payments. Each month, your company pays one amount divided into three buckets: claims funding, administrative fees, and stop-loss insurance premiums. Stop-loss protects you from catastrophic claims. The claims fund covers your employees' day-to-day medical expenses.

You know your payment every month, which makes budgeting predictable. If claims run low, you may get a portion of the unused claims fund back at year-end. If claims spike, stop-loss kicks in to cap your exposure.

Most employers in the 25 to 200 employee range find this structure fits well. Top carriers offering level-funded plans for small and midsize employers include UnitedHealthcare, Aetna, Cigna, and Anthem.

One important distinction: under a level-funded arrangement, your company is the plan sponsor under ERISA. That adds administrative responsibilities, but it also gives you access to claims data that fully insured plans typically withhold, data you can use to understand what's driving costs and make smarter benefits decisions year over year.

How Does a Level Funded Health Plan Work?

Each month, one fixed payment covers everything. It doesn't change based on whether claims were high or low that month.

The Three Components of Your Monthly Payment

The administrative fee covers the third-party administrator handling claims processing, network management, and member services. This typically runs $30 to $60 per employee per month, depending on what's included.

The stop-loss premium is what makes level funding viable for smaller employers. It protects against both individual high-cost claims and aggregate claims exceeding expected levels. Without it, a single $200,000 cancer treatment or complicated premature birth could create serious financial exposure.

The claims fund pays your employees' actual medical expenses throughout the year.

Year-End Reconciliation and Potential Refunds

At year-end, the administrator compares actual claims against what was set aside in the claims fund. If claims came in under budget, you may receive a surplus refund. Some carriers return 50% of the surplus, others return more. That potential refund is one of the main reasons employers choose this structure.

Level Funded vs. Fully Insured Plans: Key Differences

With a fully insured plan, you pay a set premium and the carrier assumes all claims risk. If your group is healthy and claims are minimal, the carrier keeps the savings. You get no refund.

A level-funded plan shifts some of that risk back to the employer, capped by stop-loss, but you capture the upside when claims run low. You also get claims data that shows exactly what's driving your healthcare spend, information that fully insured plans rarely share and that employers need to manage costs strategically.

The financial case is becoming harder to ignore. The KFF 2025 survey found average family premiums hit $26,993 this year, up 6% from 2024. Employers who stay on fully insured plans absorb that increase with no mechanism to offset it. Level funding gives you a structure where controlling utilization translates directly into lower costs.

Level Funded Health Plan Pros and Cons

Advantages

Cost savings potential is the primary draw. When claims come in under projections, you keep a portion of that money. Younger, healthier workforces tend to see the most consistent returns.

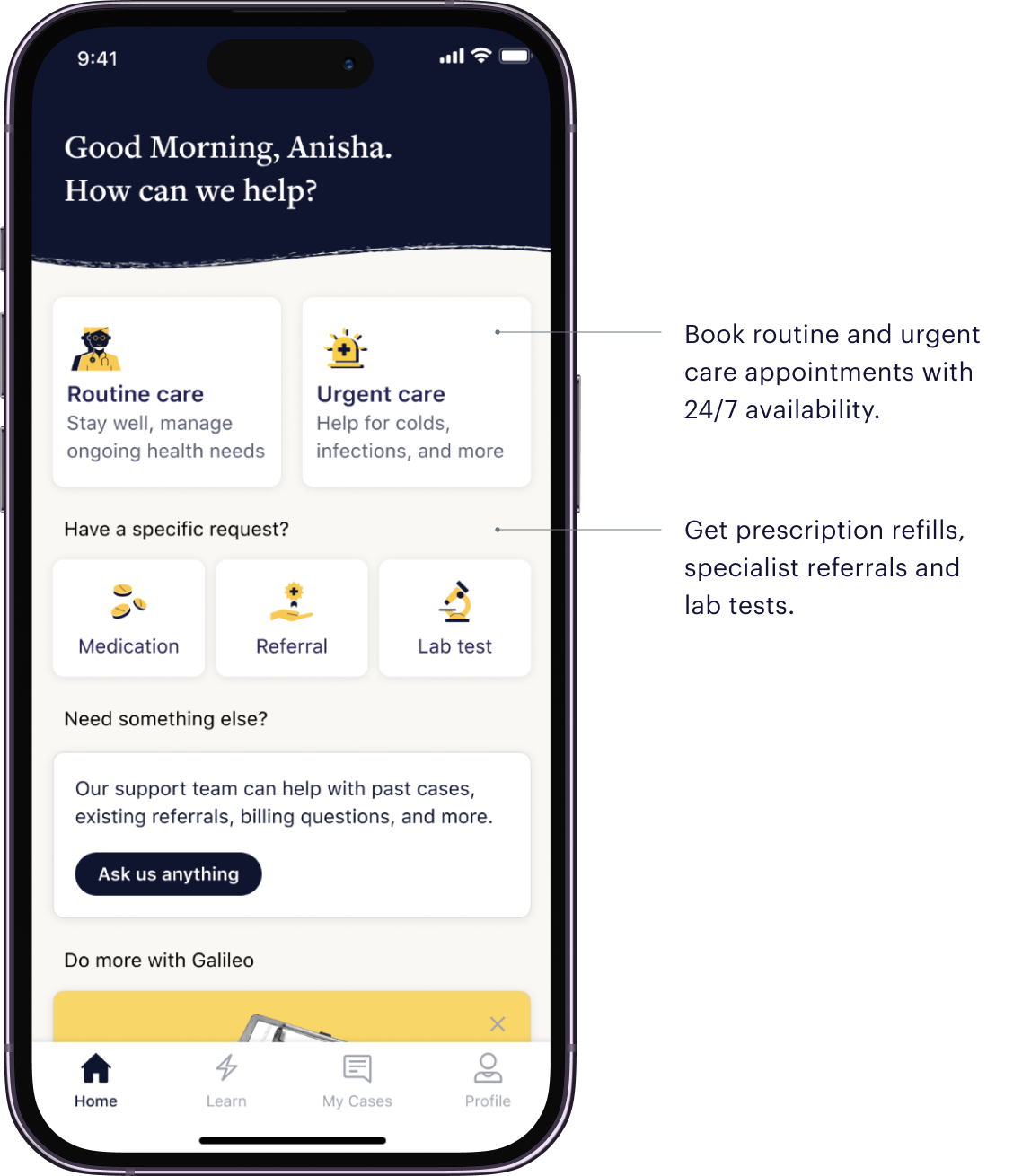

Claims transparency gives you actionable data. You'll see exactly where your healthcare dollars go, which makes it possible to address cost drivers before they compound. Employers who pair a level-funded plan with 24/7 virtual primary care access tend to see fewer avoidable ER and urgent care claims, one of the biggest cost levers under this structure.

Drawbacks

Medical underwriting can limit access or raise costs for groups with more complex health needs. A bad claims year can spike your renewal rate despite stop-loss protection. Administrative burden is higher than that of a fully insured plan. And surplus refunds aren't guaranteed. They depend on how your claims actually perform.

Who Should Consider a Level Funded Health Plan?

Companies with 25 to 200 employees are typically the best fit. Employers with healthier, younger workforces see the most consistent returns. Organizations willing to take on ERISA responsibilities and manage a third-party administrator relationship can make it work well.

Care access matters here, too. Claims costs are directly shaped by where and how employees get care. Employers who give their workforce a clear path to primary care, including 24/7 virtual access for urgent and ongoing needs, tend to see fewer avoidable claims at renewal.

Galileo works as a virtual-first primary care solution available in all 50 states, with phone, video, and chat access around the clock. Employers who've partnered with Galileo have seen an 11.5% reduction in total cost of care within six months, the kind of result that directly affects what a level-funded plan costs at renewal.

How to Tell If a Plan Is Level Funded

- Your monthly bill breaks into separate components: admin fees, stop-loss premium, and claims funding

- Stop-loss coverage documents come with the plan materials

- The contract includes year-end settlement or surplus refund language

- You have access to detailed claims reporting

- ERISA plan documents name your company as the plan sponsor and administrator

Choosing the Right Level Funded Health Plan Provider

Network adequacy should match where your workforce is located. Stop-loss terms vary significantly between carriers. Attachment points, aggregate limits, and exclusions matter more than the headline premium. Administrative capabilities affect day-to-day operations, especially claims turnaround and member support.

For employers also evaluating virtual primary care, it's worth asking whether the carrier offers integrated options or whether a dedicated solution makes more sense.

Galileo works across plan types and complements existing benefits rather than replacing them, keeping more care within primary care and reducing the high-cost claims that hit hardest under a level-funded structure. See how Fortune Brands applied this approach across a distributed workforce.

.webp)

.webp)

.webp)

.webp)

%20(1).webp)

%20(1).webp)

.webp)